Understanding Education Loans

Education loans are financial products specifically designed to assist students in covering the costs associated with higher education, including tuition fees, accommodation, and materials. These loans play a pivotal role in enabling individuals to pursue their academic aspirations, particularly in cases where personal finances do not suffice to meet educational expenses.

There are two principal types of education loans: federal and private loans. Federal education loans are funded by the government and offer benefits such as fixed interest rates, income-driven repayment options, and potential loan forgiveness programs. These loans typically have more favorable repayment terms and a higher level of flexibility compared to private loans. Examples include Direct Subsidized Loans and Direct Unsubsidized Loans, which cater to both undergraduate and graduate students.

On the other hand, private education loans are issued by private financial institutions like banks and credit unions. These loans are not governed by federal regulations, resulting in a wider variance in interest rates and repayment terms. Private loans often require a credit check, and their rates can be influenced by the borrower’s creditworthiness. Generally, borrowers might consider private loans when federal options do not cover the entire cost of education.

Eligibility for education loans varies, but certain criteria are commonly considered. For federal loans, students typically need to complete the Free Application for Federal Student Aid (FAFSA) and demonstrate financial need. Private lenders often require proof of income or a cosigner to secure a loan. It is important for borrowers to assess their financial situation carefully to determine the most suitable type of loan.

In this context, education loans serve not only as a means to finance one’s college education but also as a crucial investment in the future, influencing career opportunities and earning potential.

Assessing Your Financial Needs

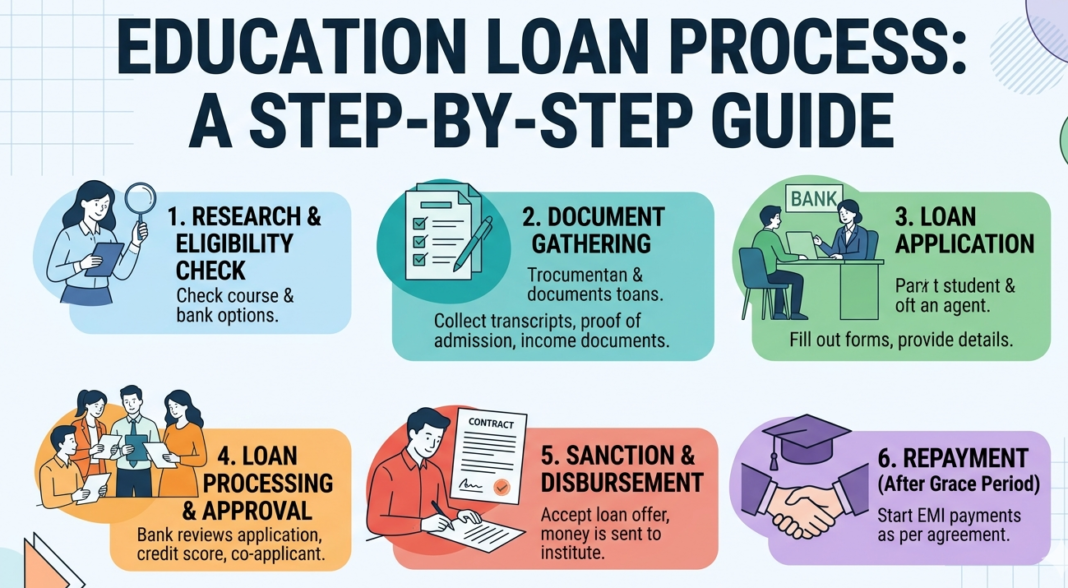

When considering an education loan, the first critical step is to assess your financial needs thoroughly. This evaluation involves taking into account various factors, including tuition fees, living expenses, and other education-related costs. By understanding these expenses, you can calculate the total amount needed to borrow efficiently.

Start by compiling the tuition charges for your chosen institution. Different programs may have varying fees, so it is essential to have precise figures. Most universities provide an estimated cost of attendance that includes tuition as well as additional required fees. This will form a significant portion of the overall financial needs.

Next, consider your living expenses. These typically encompass accommodation, food, transportation, and miscellaneous costs. Depending on your lifestyle and location, these expenses can vary significantly. It may be beneficial to research average costs in the area where you will be studying and create a budget that accurately reflects your anticipated living situation.

In addition to tuition and living costs, factor in other education-related fees. These can include textbooks, supplies, health insurance, and technology requirements, such as laptops or software. Estimating these costs is crucial as they can accumulate and impact your overall loan amount. You may also want to include any one-time fees, such as orientation or registration charges that your institution may impose.

Once you have gathered all this information, tally your expenses to arrive at a comprehensive figure. This calculated total will provide clarity on how much you need to borrow through an education loan. By carefully evaluating your financial needs, you can avoid borrowing more than necessary and ensure a focused approach to financing your education.

Exploring Loan Options

When considering financing options for education, borrowers typically encounter a variety of education loans, each with distinct features. Education loans can be broadly categorized into federal and private loans. Understanding the differences between these options is essential for making informed decisions regarding funding your educational journey.

Federal education loans, often considered the most advantageous, are funded by the government and come with benefits such as lower interest rates and more flexible repayment terms. The most common types of federal loans include Direct Subsidized Loans, Direct Unsubsidized Loans, and Direct PLUS Loans. Subsidized loans offer the added benefit of interest coverage during the borrower’s time in school, whereas unsubsidized loans begin accruing interest immediately. Importantly, federal loans typically offer borrower protections like deferment and forgiveness programs based on income, making them a preferred choice for many students.

On the other hand, private education loans are offered by banks, credit unions, and other financial institutions. These loans generally have higher interest rates than federal loans, which can vary significantly based on creditworthiness. Unlike federal loans, private loans often require a credit check and may involve a co-signer. Repayment terms can also differ, with some lenders providing more rigid structures than federally regulated loans. It is crucial for borrowers to review the terms closely, as private loans typically lack the extensive repayment options and borrower protections afforded by federal programs.

In summary, while both federal and private education loans can provide necessary funding, prospective borrowers should evaluate their specific circumstances, including credit history and financial needs, to determine the most suitable option. Taking the time to understand the nuances of each type of education loan can significantly impact the overall financial health of students post-graduation.

Researching Lenders

Choosing the right lender for your education loan is a crucial step that can significantly impact your overall financial burden during and after your studies. The first aspect to consider is the reputation of the lender. It is advisable to seek lenders who have a proven track record in providing educational loans. Reviews and testimonials from previous borrowers can offer valuable insights regarding their experiences with the lender’s services. Additionally, verify the credentials of the institution to ensure they are reputable and authorized to provide educational loans.

Customer service is another key factor to evaluate while selecting a lender. Effective and efficient customer service can facilitate the loan application process and provide assistance throughout the repayment phase. Look for lenders that offer various communication channels, such as phone support, live chat, and email to ensure that their services are easily accessible. It is also beneficial to assess their responsiveness during the research phase; quick responses to your inquiries can indicate the lender’s commitment to customer satisfaction.

Loan terms are equally important when it comes to selecting a lender. Different lenders offer varying interest rates, repayment terms, and fees associated with their loans. A careful review of these terms will help you accurately compare the cost of borrowing from different institutions. Be wary of any hidden charges or prepayment penalties that might increase the overall expense of the loan. Prioritize lenders with flexible repayment options, including deferment and forbearance provisions, which can provide essential relief during instances of financial hardship.

By adopting a thorough approach to researching lenders, you can make an informed decision that aligns with your educational finance needs, ultimately contributing to a more manageable repayment experience.

Gathering Necessary Documentation

Applying for an education loan involves several steps, one of which is gathering the necessary documentation. A well-prepared application can significantly enhance your chances of obtaining the required funds. First and foremost, you will need to provide proof of identity, which typically includes government-issued identification, such as a passport, driver’s license, or national ID card. This documentation helps the lender confirm your identity and assess your credibility.

In addition to identification, proof of income is essential. This may include salary slips, bank statements, or tax returns for the past few years. If you are a student, you may not have an income, but if you are currently employed, providing your income details is crucial. Furthermore, credit history plays a vital role in the loan application process. You should gather documents that reflect your credit score and any previous loans you may have taken out, as they give lenders insight into your financial reliability.

Moreover, an acceptance letter from the educational institution you plan to attend is a vital piece of documentation. This letter confirms that you have been offered a place in a course, which is often a prerequisite for securing educational financing. Some lenders may also require additional documents such as a list of courses and their associated costs, especially if the program lasts several years.

Being organized and having all necessary documentation ready can streamline your education loan application process. It not only speeds up processing time but also demonstrates your preparedness and seriousness about your educational goals. Remember, each lender may have specific document requirements, so verify with them to ensure you have everything necessary.

Filling Out the Loan Application

When embarking on the journey to secure an education loan, understanding how to fill out the loan application correctly is crucial. This process typically involves deciding whether to apply online or in person. Many borrowers today prefer the convenience of online applications due to their accessibility, but in-person applications can provide immediate clarification of doubts by interacting directly with loan officers.

Before starting the application, gather necessary documents such as proof of income, identification, and educational details. This ensures that you have all relevant information ready, minimizing delays in the application process. When filling out the application, be meticulous. Accurate information is paramount, as discrepancies can lead to loan denial or repayment issues later on.

While filling out the application, pay attention to common pitfalls that applicants often encounter. For instance, ensure that personal information, such as your name and social security number, is entered accurately to avoid any discrepancies. Double-check numerical entries, particularly when reporting income or expenses. In some cases, minor mistakes can raise red flags or lead to lengthy verification processes.

After completing the application, review it thoroughly before submission. Look for incomplete sections or misunderstood questions that may hinder acceptance. Seeking assistance from family members or financial advisors can provide additional clarity and help avoid common mistakes. Most lenders offer customer service for queries—utilize these resources if uncertainties arise.

In summary, filling out an education loan application is a vital step that requires careful attention to detail. By applying online or in person, ensuring accuracy, and reviewing your information, you can streamline the loan acquisition process and increase your chances of securing the necessary funds for your education.

Understanding Approval Processes

When applying for an education loan, understanding the approval process is essential. This process often begins with a thorough evaluation of the applicant’s credit history. Lenders typically conduct a credit check to assess the creditworthiness of the borrower, as a strong credit score can significantly influence the terms of the loan, including interest rates and repayment plans.

In addition to the credit check, financial circumstances play a pivotal role in the approval process. Lenders will evaluate the applicant’s income, employment stability, and existing debts. This evaluation helps the lender determine the applicant’s ability to repay the loan responsibly. It’s advisable for applicants to gather all essential documentation, such as proof of income and existing liabilities, to facilitate a smoother approval process.

The timeline for receiving approval can vary depending on the lender and the complexity of the application. Generally, applicants can expect to wait anywhere from a few days to several weeks. During this period, lenders may request additional information or documentation. It is important for applicants to remain proactive and responsive to any communications from the lender to avoid delays.

In cases where a loan application is denied, it is crucial for the applicant to seek feedback from the lender. Understanding the reasons for denial, whether it be due to low credit score or insufficient income, allows applicants to take appropriate measures to improve their financial profile. Applicants can consider improving their credit score, reducing existing debt, or seeking a co-signer to enhance their chances of approval in the future.

Repayment Plans and Options

When it comes to paying back education loans, borrowers are presented with several repayment plans designed to cater to their individual financial situations. Understanding these options is crucial in managing your debt effectively and ensuring that you stay on track financially.

One of the most popular choices is the income-driven repayment plan. These plans cap your monthly payments at a percentage of your discretionary income, making them a great choice for those who may be facing financial hardships or have lower income levels. This type of plan not only makes monthly payments more manageable but may also lead to loan forgiveness after a certain period, typically 20 to 25 years, depending on the specific plan.

Another option to consider is loan consolidation. Consolidating your loans can simplify repayment by combining multiple loans into a single loan with a fixed interest rate. This can lower your monthly payments and give you the convenience of a single payment. However, borrowers should carefully assess whether consolidation is the best option, as it can sometimes lead to a longer repayment term and more interest paid over time.

Additionally, some borrowers may qualify for deferment or forbearance. Deferment allows borrowers to temporarily stop making payments on their loans without accruing interest, provided they meet certain criteria. Forbearance offers a similar break but does accrue interest during the period of non-payment. Both options can be beneficial during times of financial difficulty, but it is essential to understand the long-term implications of these choices.

Choosing the right repayment plan requires careful consideration of your financial situation, future income potential, and the specific terms of your education loans. It is advisable to consult with a financial advisor or loan servicer to ensure that you are well-informed about the available options and their respective benefits and drawbacks.

Managing Your Education Loan After Disbursement

Once your education loan has been disbursed, the management of these funds becomes crucial for both your financial health and academic success. Effective money management starts with creating a detailed budget that outlines your expected expenses, including tuition fees, housing, textbooks, and other educational materials. By carefully tracking your expenditures against this budget, you can ensure that your loan money lasts throughout your academic term.

In addition to budgeting, monitoring your expenses plays a significant role in effective loan management. Consider utilizing various tools or applications designed for budget tracking; these can help you categorize your spending and keep an eye on where your money is going. An organized approach to expenses will provide clarity and allow you to adjust your spending habits as necessary, thereby minimizing financial strain.

It is also important to understand how interest accrual will affect your education loan. Most education loans accrue interest while you are studying, which adds to the total amount you will owe once the repayment period begins. Familiarizing yourself with the terms of your loan agreement will clarify when interest starts accruing and at what rate. This knowledge can help you make informed decisions about making interest payments while still in school if your budget allows.

Furthermore, preparing for repayment should be an integral part of your financial strategy. Start building a plan early by researching your repayment options, including alternative repayment plans or loan forgiveness programs. This foresight can reduce stress and lead to more manageable repayments once you graduate. Keeping lines of communication open with your lender throughout the loan period is also advisable, as they can offer guidance and information relevant to your financial situation.

{kind=link}